F&M Bank Chief Credit Officer offers insight on the current state of commercial lending

F&M Bank Chief Credit Officer offers insight on the current state of commercial lending

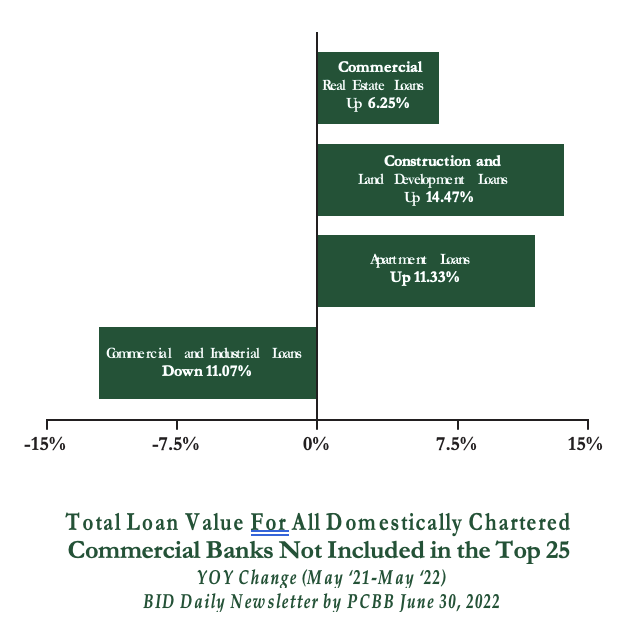

Q: Describe the commercial lending landscape for the first half of 2022.

A. Demand for commercial lending has increased. Businesses that closed during the pandemic were able to rebound last year, resulting in the highest number of new business applications ever filed in 2021, according to the Census Bureau. Commercial real estate loans, construction and land development loans, and apartment loans also increased year over year. I expect during the second half of 2022, commercial lending will level out.

Q: What has been the impact of the Federal Reserve’s 0.75% rate increase, the largest increase we’ve seen in nearly 30 years?

A. The short answer: it’s more expensive to borrow money; however, it’s much more complicated than that. CRE owners who are selling or refinancing properties are seeing the highest valuations ever. Despite recession concerns, owners still have maturing loans and are considering taking cash out of their properties while values are still high. Many believe that if a recession occurs, rates will have to drop again, so they are opting for shorter-term fixed rates that are relatively attractive.

A. One trend we’ve seen recently is an increase in purchase transactions via 1031 exchanges. Property owners are being offered record high prices from large institutional buyers, including real estate funds looking for commercial space (e.g. retail, distribution, etc.). Sellers are jumping at these opportunities but then need to find another property due to tax implications related to the original sale. F&M’s Relationship Managers are skilled at crafting cash flows and structures amenable to 1031 exchanges.

Q: Has construction activity returned to pre-pandemic levels?

A. Supply chain issues continue to affect developers of ground-up construction and owners desiring to make tenant improvements. However, this should correct itself over time.

Q: Is F&M Bank still making loans?

A: Yes, our Relationship Managers are busy handling commercial loan requests. Unlike other banks whose pricing is tied to the 10-Year Treasury Note, F&M tailors its pricing to the overall relationship, which tends to be better priced in a rising rate environment. Except in rare instances, we do not sell or participate in our commercial loans in the secondary market. When a commercial loan client enters into a relationship with F&M, we are in it for the long haul. F&M is still issuing loans and is willing to be creative.

Phil Bond, Executive Vice President and Chief Credit Officer at Farmers & Merchants Bank, a 115-year-old regional bank based in Long Beach. For more information, visit FMB.com. All loans are subject to co-credit approval. • NMLS #537388 • Member FDIC

Phil Bond, Executive Vice President and Chief Credit Officer at Farmers & Merchants Bank, a 115-year-old regional bank based in Long Beach. For more information, visit FMB.com. All loans are subject to co-credit approval. • NMLS #537388 • Member FDIC